{kind=link}

Strategy’s enterprise mNAV dipping below 1 marks a critical moment for the corporate Bitcoin model, as the market values the entire structure at less than its Bitcoin holdings, raising questions about sustainability.

🔑 Key Takeaways

- Strategy’s enterprise mNAV falls below 1 for the first time, indicating market value is less than Bitcoin holdings.

- STRC preferred stock trades at a 26% discount to par, impairing funding mechanisms.

- Annual dividend obligations have quadrupled to $1.2 billion, straining cash reserves.

- CryptoQuant recommends pausing Bitcoin purchases to rebuild cash reserves.

- The crisis affects the entire corporate Bitcoin treasury model, with competitors also trading below parity.

The Anatomy of the Crisis: How Strategy’s Funding Machine Broke Down

Strategy holds approximately 847,363 BTC at an average cost of $75,577 per coin, representing 3.8% of Bitcoin’s circulating supply. Its software business generates about $320 million in annual gross profit, insufficient for preferred share dividends. The company relies on STRC perpetual preferred shares for funding, which adjusts dividends to maintain a $100 par value.

The STRC instrument was designed as a self-correcting mechanism, but with Bitcoin falling from over $100,000 to mid-$50,000, STRC now trades at approximately $74. This discount makes new issuance dilutive and has caused the funding flywheel to malfunction.

The model relies on a virtuous cycle: Bitcoin rises, STRC stays near par, Strategy raises cheap capital, buys more Bitcoin, pays dividends from new issuance proceeds, and repeats. With Bitcoin declining, this cycle has reversed.

Dividend Obligations Quadruple as Cash Reserves Hemorrhage

Annual dividend obligations have surged from approximately $300 million at the start of 2026 to around $1.2 billion today, primarily due to massive STRC and other preferred share issuance. Current cash reserves stand at approximately $1.4 billion, providing only 14 months of coverage, down from over 7 years when obligations were $300 million.

In June 2026, Strategy conducted its first standalone Bitcoin sale since 2022, disposing of 32 bitcoin specifically to fund preferred share dividends. This distress sale marks a philosophical rupture for a company built on the principle of never selling Bitcoin.

Available options for Strategy are limited: drawing down cash reserves, selling more Bitcoin, or diluting common shareholders through new equity issuance. None are attractive, as each would accelerate financial deterioration.

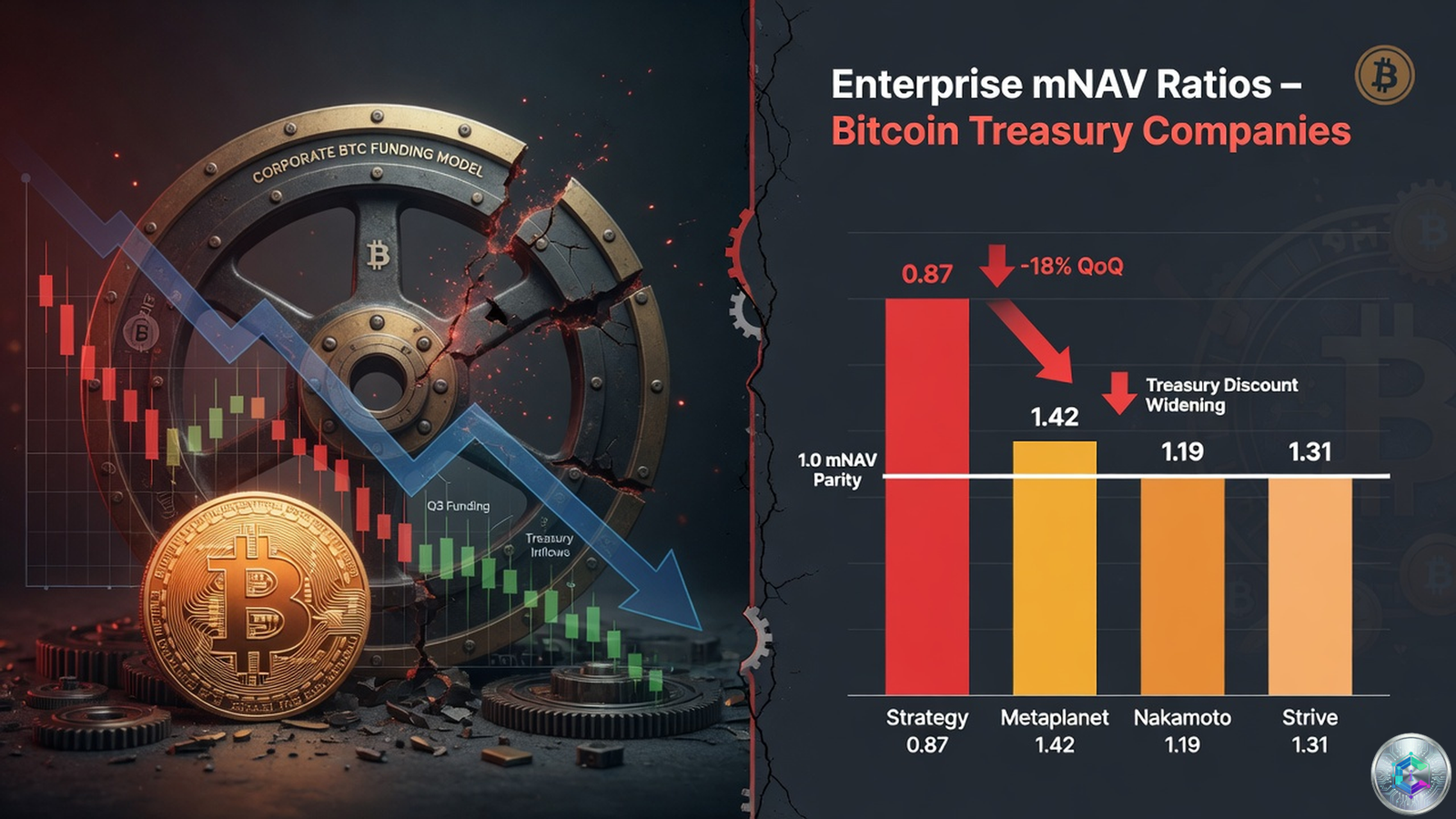

The mNAV Below 1: What It Means and Why It Matters

Enterprise mNAV is calculated by dividing total market capitalization by the market value of Bitcoin holdings, adjusted for net debt and obligations. A ratio above 1 indicates a premium assigned to the corporate structure, management expertise, and funding model. In late 2024, Strategy’s mNAV traded as high as 2.6x to 2.8x, meaning the market valued the company at nearly three times its Bitcoin holdings.

The collapse of that premium has been swift and severe. By June 2026, several similar companies also trade below parity, suggesting a broader reassessment of the corporate Bitcoin treasury model.

| Company | Enterprise mNAV | Status |

|---|---|---|

| Strategy | Below 1.0 | Below Parity |

| Metaplanet | 0.9 | Below Parity |

| Nakamoto | 0.92 | Below Parity |

| Strive | 1.24 | Above Parity |

Strive: The Exception That Proves the Rule and STRC’s Correlation

Strive trades at an mNAV of approximately 1.24, maintaining a premium due to simpler capital structure or management credibility. Meanwhile, STRC’s 90-day correlation with Bitcoin has risen to 0.70, its highest level since launch, undermining its appeal as an income vehicle.

STRC was designed to provide stable income decorrelated from Bitcoin volatility, but this decorrelation has disappeared, raising questions about dividend funding sustainability through new capital inflows.

CryptoQuant Sounds the Alarm: Rebuild Cash Reserves

CryptoQuant published a report recommending Strategy immediately pause Bitcoin purchases and focus on rebuilding cash reserves to approximately $2.8 billion for 24 months of dividend coverage. CryptoQuant CEO Ki Young Ju characterized Strategy’s ongoing Bitcoin purchases as a « liquidity sink » rather than a growth driver.

« Strategy’s ongoing bitcoin purchases in the current market environment are a ‘liquidity sink’ rather than a growth driver. »

Ki Young Ju, CEO of CryptoQuant

Critics like Peter Schiff and Brad Garlinghouse have highlighted risks in the STRC structure and impact on the broader Bitcoin market.

What Comes Next: Scenarios for Strategy’s Future

Three scenarios are possible: a managed contraction where Strategy halts Bitcoin purchases and rebuilds reserves; continued accumulation despite pressure, based on long-term conviction; or fundamental capital restructuring, involving preferred share renegotiations.

As the largest corporate Bitcoin holder, Strategy’s decisions have disproportionate market impact. Potential Bitcoin sales to cover dividends could exert significant pressure, as would cessation of purchases.

The relationship between Strategy and the Bitcoin market has always been circular: willingness to buy at a premium supported prices, but with assumptions challenged, this logic turns against the company.

Conclusion

Strategy’s crisis underscores the dangers of embedding excessive leverage into a volatile asset. While the corporate Bitcoin treasury model may be valid long-term, short-term financial engineering creates fragility when assumptions change. The market’s verdict signals a need for reassessment for institutional and retail investors.

Lessons from this situation warn against promises of permanent premiums and highlight the importance of financial discipline in corporate Bitcoin accumulation.

Sources

- The Block – Strategy loses its bitcoin premium as enterprise mNAV dips below 1 (June 26, 2026)

- CoinDesk – STRC’s correlation with BTC hits record high (June 25, 2026)

- Yahoo Finance – Strategy Halts STRC Sales and Sells Bitcoin to Cover Dividends (June 22, 2026)

- CryptoQuant – Analysts Say Strategy Should Pause Bitcoin Purchases (June 24, 2026)

- Bitcoin Magazine Pro – STRC Explained (April 16, 2026)

This article is published for informational and educational purposes only. It does not constitute investment advice. Conduct your own research (DYOR) before making any decisions.