{kind=link}

Morgan Stanley Launches Bitcoin ETF With the Lowest Fee Structure in the Market, Acquires 430 BTC on Opening Day

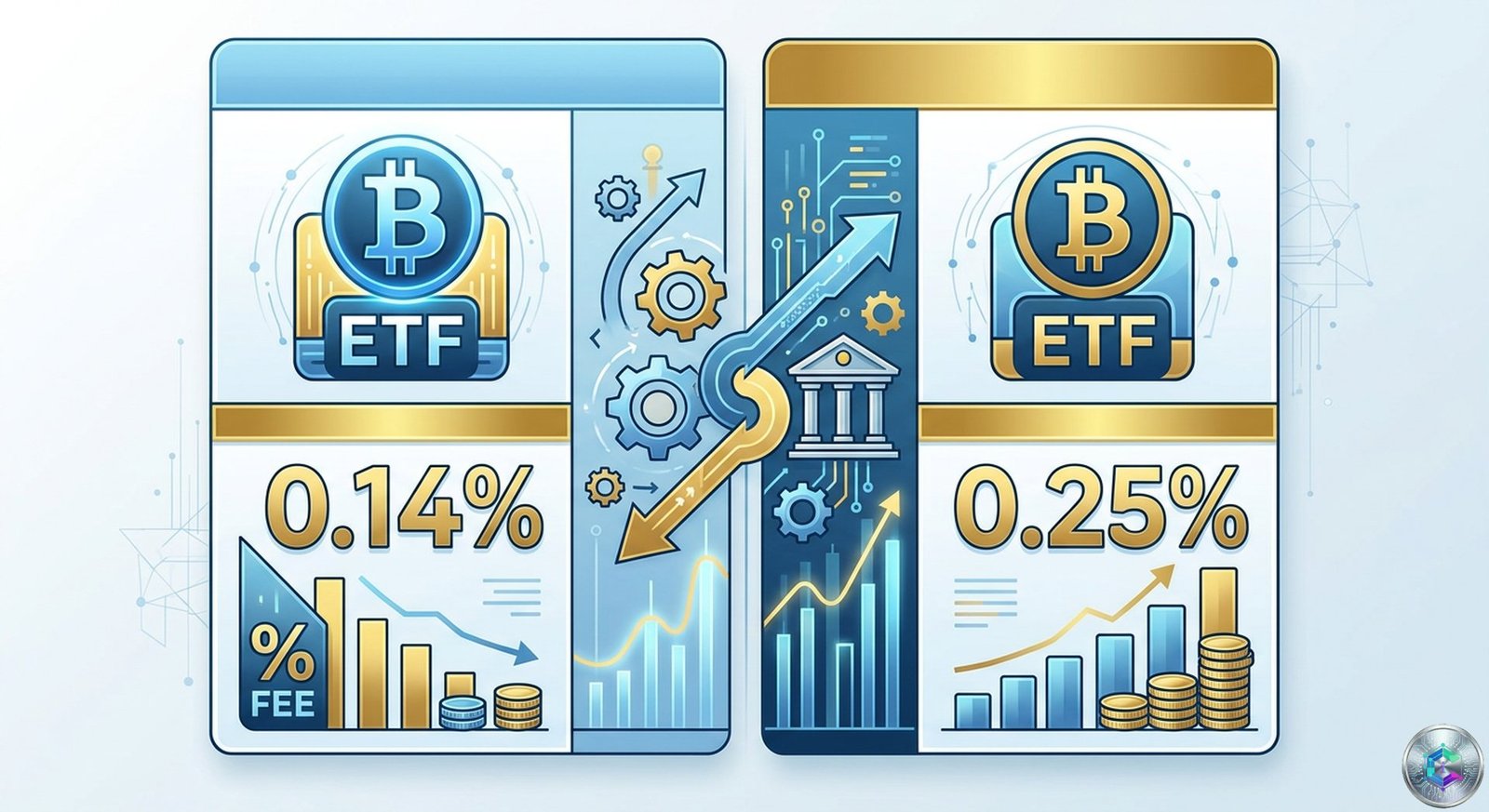

Morgan Stanley has officially entered the Bitcoin exchange-traded fund market with a product that is already reshaping the competitive dynamics of digital asset investment. The Morgan Stanley Bitcoin Trust, trading under the ticker MSBT on the New York Stock Exchange, launched on April 8, 2026, with an expense ratio of just 0.14 percent — the lowest fee among all spot Bitcoin ETFs currently available in the United States. The debut immediately intensified competitive pressure on BlackRock’s dominant IBIT fund, which charges 0.25 percent, and triggered widespread speculation throughout the financial industry about how institutional capital will flow into this new vehicle.

Within hours of the opening bell, blockchain data analysis revealed that the MSBT trust had already accumulated approximately 430 Bitcoin, worth roughly $29 million at prevailing market prices. That initial acquisition signaled strong internal conviction at Morgan Stanley despite a challenging broader market environment in which Bitcoin had experienced significant volatility and price decline in the preceding weeks. The timing of the launch — directly into a downturn rather than during a period of rising prices — was interpreted by market analysts as a deliberate signal that the firm views current valuations as an attractive entry point for long-term institutional allocation rather than a reason to delay deployment.

A Pricing Revolution in the Bitcoin ETF Space

The 0.14 percent expense ratio is not merely a pricing footnote. It represents a calculated strategy to compete on cost efficiency at a stage when Bitcoin ETFs have become a mature product category with over $85 billion in combined assets under management across all issuers. Before Morgan Stanley entered the market, the Bitcoin ETF landscape was already crowded with offerings from BlackRock, Fidelity, Franklin Templeton, Valkyrie, and Ark Invest, among others. None of those products, however, brought the distribution advantages that Morgan Stanley commands through its wealth management platform — one of the largest networks of affluent clients and high-net-worth individuals in the United States and internationally.

Morgan Stanley Wealth Management oversees approximately $9.3 trillion in client assets and employs roughly 16,000 financial advisors across the country. While the firm had previously allowed certain advisors to recommend third-party Bitcoin ETF exposure to qualified clients as of August 2024, the launch of a proprietary product fundamentally transforms the economics and incentives of that distribution model. When an advisor recommends the Morgan Stanley Bitcoin Trust to a client, the capital stays within the Morgan Stanley ecosystem rather than flowing toward competing products from BlackRock or Fidelity. That internal alignment creates a structural commercial advantage that no third-party Bitcoin ETF provider can replicate.

Bloomberg senior ETF analyst Eric Balchunas described the MSBT debut as landing in the top one percent of all ETF launches in terms of initial demand metrics. That assessment, delivered within hours of the trading debut, reflected not just the volume of initial subscriptions but the quality of the investor base — a composition that includes high-net-worth individuals, family offices, and institutional accounts that typically exhibit lower churn and longer holding periods than retail-dominated products. The difference between a product that attracts long-term strategic buyers versus one that draws speculative short-term traders can determine the long-term trajectory of an ETF’s asset accumulation.

Why This Launch Differs From the First Generation of Bitcoin ETFs

Spot Bitcoin ETFs existed for nearly two years before Morgan Stanley entered the market. The initial cohort of products, launched in January 2024 after the Securities and Exchange Commission approved multiple applications following years of regulatory resistance, accumulated substantial assets but faced an uneven reception among institutional investors and wealth management platforms. Many advisory firms moved slowly to approve Bitcoin ETF exposure for client accounts, and advisors frequently faced internal compliance scrutiny when recommending digital asset products to clients.

Morgan Stanley’s approach differs in several fundamental respects. First and most visibly, the firm is the first major U.S. bank to launch its own spot Bitcoin ETF. That distinction carries regulatory and reputational weight that pure asset management competitors cannot match. As a bank operating under the oversight of multiple federal regulators, Morgan Stanley has navigated a more complex compliance framework to bring this product to market. The internal risk management and legal review processes that precede a product launch of this nature are substantially more rigorous than those faced by non-bank ETF sponsors. Second, the seamless integration with existing Morgan Stanley advisory relationships means prospective buyers do not need to open new brokerage accounts, complete additional KYC processes, or navigate unfamiliar technology platforms — the Bitcoin trust is available within the existing Morgan Stanley client experience.

The firm’s published guidance from November 2024, which suggested that clients allocate as much as 4 percent of their portfolio to Bitcoin, served as a public signal that Morgan Stanley was building toward deeper engagement with digital asset exposure. That recommendation, combined with the April 2026 product launch, represents the execution of a strategic roadmap that industry observers had anticipated for months. The stated expansion plans for Solana and Ethereum trusts indicate that Morgan Stanley views the Bitcoin ETF as merely the first component of a broader multi-asset digital asset product suite — a more ambitious vision than a single-product entry into a trendy market segment.

The Competitive Threat to BlackRock’s IBIT Dominance

BlackRock’s IBIT currently commands the largest share of the Bitcoin ETF market, with over $53 billion in net assets as of early 2026. The fund has been remarkably successful since its January 2024 launch, consistently attracting net inflows even during periods of Bitcoin price weakness and broader crypto market volatility. The firm’s iShares brand carries enormous weight among financial advisors and institutional investors, and the operational infrastructure behind IBIT — including custody arrangements with Coinbase — is widely regarded as best-in-class.

However, the Morgan Stanley entry introduces a competitive dynamic that IBIT has not previously faced. Financial advisors working within the Morgan Stanley platform can now recommend a proprietary Bitcoin product with lower fees and immediate integration into existing client portfolios, eliminating the friction that comes from directing clients to an external fund provider. In a relationship-driven wealth management business, that friction matters more than pure cost considerations for many advisors and clients.

The fee differential of 0.11 percentage points may seem modest in percentage terms, but over large portfolio allocations it translates into meaningful cost savings over time. For a client with a $500,000 allocation to Bitcoin through an ETF, the annual fee difference between IBIT and MSBT amounts to approximately $550 per year. On a $5 million portfolio, that same differential grows to $5,500 annually. For wealth management clients who hold positions across multi-year time horizons, the cumulative cost advantage of the lower-fee product becomes increasingly significant and will likely influence allocation decisions as assets grow.

BlackRock had not announced fee reductions as of early April 2026 in response to the Morgan Stanley launch, though industry observers widely expect the asset management giant to evaluate its pricing strategy given the changed competitive landscape. Fidelity’s Bitcoin ETF currently charges 0.25 percent, matching BlackRock’s structure, and several other issuers operate in the same general fee range. The key question occupying market participants is whether the Morgan Stanley entry triggers a broader fee war across the Bitcoin ETF industry or whether competitors choose to differentiate on non-price factors such as fund size, trading liquidity, track record, and operational infrastructure.

Institutional Capital Deployment and Market Implications

The broader significance of the Morgan Stanley launch extends beyond direct competitive pressure on existing Bitcoin ETF providers. The event represents a milestone in the ongoing institutionalization of Bitcoin as an asset class. The original cryptocurrency was created in 2009 as a peer-to-peer electronic cash system described in a white paper published by the pseudonymous Satoshi Nakamoto. For much of its early history, Bitcoin was associated with cypherpunks, retail speculators, libertarians, and fringe financial actors who sought alternatives to government-issued currencies. The past several years have witnessed a dramatic transformation in who holds Bitcoin and why they hold it.

Regulatory approvals for spot Bitcoin ETFs, improvements in custodial infrastructure, and the entry of firms like Morgan Stanley have collectively moved Bitcoin from the margins of the financial system toward its center. The firm manages $6.2 trillion in total client assets, a figure that dwarfs the entire Bitcoin market capitalization, which currently stands at approximately $1.3 trillion. Even a modest percentage allocation by the firm’s wealth management clients to Bitcoin through the MSBT product would represent billions of dollars in new market demand. The natural holding period for ETF-based Bitcoin exposure tends to be measured in years rather than months or weeks, a structural characteristic that reduces the intensity of selling pressure during price downturns relative to what might be observed among retail traders on cryptocurrency exchanges.

The capital flowing into Bitcoin ETFs through vehicles like MSBT is not intended for short-term trading. Industry participants have repeatedly emphasized that the appropriate investment horizon for these products is measured in years, not quarters. That long-term orientation matters for market dynamics because it theoretically reduces price volatility over extended periods. When Bitcoin prices fall, long-term institutional holders using ETF structures face higher transaction costs and tax implications from selling than from holding — factors that create natural price support during market stress.

The Regulatory Landscape and Future Expansion Plans

The launch of MSBT occurs against a backdrop of evolving regulatory guidance for digital assets in the United States. The SEC under its current leadership has adopted a more permissive approach to crypto-related financial products than previous administrations, clearing the path for spot Bitcoin ETF approvals that seemed politically implausible just a few years earlier. However, the regulatory framework for stablecoins, tokenized securities, decentralized finance protocols, and broader digital asset custody remains incomplete, creating ongoing uncertainty for firms seeking to expand beyond Bitcoin into adjacent digital asset categories.

Morgan Stanley’s stated intention to launch Solana and Ethereum trusts represents a continuation of the same product development philosophy that produced MSBT. These additional trusts, if approved by regulators and brought to market, would create a multi-asset digital asset platform operating within Morgan Stanley’s existing compliance infrastructure. The timeline for those expansions remains uncertain and depends on regulatory approvals that cannot be assumed. Solana and Ethereum face different regulatory classification questions than Bitcoin, which has been definitively classified as a commodity rather than a security by the Commodity Futures Trading Commission. That classification distinction matters significantly for ETF approval timelines.

The Bitcoin market has faced meaningful headwinds in recent weeks, with prices declining substantially from their late-2025 highs amid geopolitical tensions in the Middle East and broader concerns about global liquidity conditions. The Morgan Stanley launch into this challenging environment is itself a statement about the firm’s long-term conviction. Rather than waiting for a more favorable market moment to debut the product, the firm chose to enter when Bitcoin prices are suppressed — a strategy that aligns with the behavior of value-oriented institutional investors who tend to be buyers when high-quality assets trade at discounts to their assessment of intrinsic value.

What This Means for the Broader Cryptocurrency Ecosystem

The significance of a Wall Street institution as prominent as Morgan Stanley launching a Bitcoin product extends beyond the direct effects on pricing and capital flows. It represents a form of final validation for digital assets within the traditional finance establishment. When a firm with the reputation, regulatory sophistication, and client base of Morgan Stanley decides that Bitcoin exposure belongs in its product lineup, it effectively neutralizes one of the last institutional objections to cryptocurrency adoption — namely, the argument that reputable financial institutions do not offer these products to their clients.

For retail investors and smaller institutions who have observed the institutionalization of Bitcoin from the sidelines, the Morgan Stanley launch provides additional confidence that digital assets are establishing permanent infrastructure within mainstream finance. The availability of a Morgan Stanley Bitcoin product also creates a reference point and competitive benchmark for other financial institutions that may be evaluating their own digital asset strategies. If the MSBT product performs well in terms of client adoption, risk management outcomes, and regulatory relationships, it will almost certainly accelerate the strategic planning timelines for competing institutions that have been considering but not yet committed to Bitcoin product development.

The immediate competitive pressure on BlackRock is real but limited in the near term. IBIT has a two-year head start and $53 billion in assets, and switching costs for existing ETF investors are low but not trivially so. Advisors who have already built allocation frameworks and client education materials around IBIT are unlikely to move immediately to MSBT solely on the basis of a fee difference, particularly when BlackRock’s operational infrastructure and brand recognition carry significant weight. However, new capital — and Morgan Stanley advisors oversee substantial quantities of new client assets each year — will be directed toward products that offer the best combination of cost, service integration, and long-term alignment. MSBT has structural advantages that position it to capture a disproportionate share of that new capital flow.

The digital asset ecosystem stands at an inflection point where regulatory clarity, institutional adoption, and product innovation are converging to create conditions that would have seemed implausible a decade ago. Morgan Stanley’s entry into the Bitcoin ETF market represents the most visible manifestation of that convergence in early April 2026, but it is unlikely to be the last development of its kind. As more traditional financial institutions evaluate their positions in the digital asset landscape, the boundaries between cryptocurrency and conventional finance will continue to blur. The launch of MSBT functions simultaneously as a product introduction, a competitive challenge to incumbent ETF providers, and a marker of how far Bitcoin has traveled from its origins as an experiment in decentralized electronic cash toward an asset class that major banks are willing to offer as a core component of their wealth management platforms.