{kind=link}

The announcement of a stablecoin consortium involving Visa, Mastercard, Stripe, and Coinbase has shaken the market, directly threatening Circle’s business model and its USDC stablecoin. This analysis delves into the mechanics of reserve revenue, the strategic logic of card networks, and the regulatory landscape that enables this shift.

🔑 Key Takeaways

- A consortium of payment giants is reportedly planning a shared stablecoin platform.

- Reserve revenue from stablecoins, derived from Treasury bills, is at the heart of the battle.

- The GENIUS Act has created a clear regulatory framework, facilitating institutional entry.

- Circle, the issuer of USDC, is the most exposed incumbent to this competition.

- The distribution advantage of card networks could redefine the market.

The Stablecoin Reserve Economy: Where the Real Money Lives

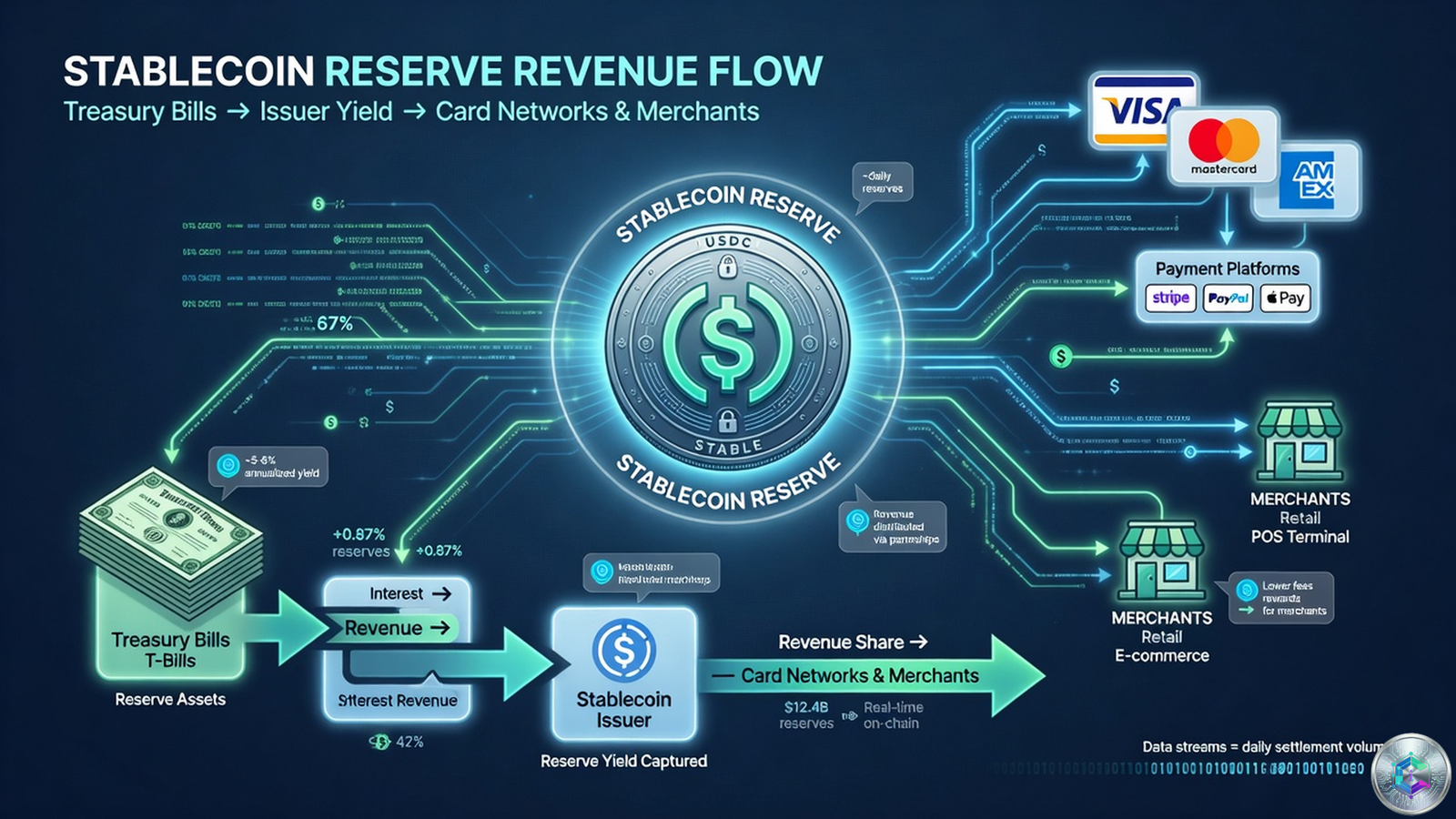

To understand the intensity of traditional finance’s interest in stablecoins, it helps to examine how these assets actually generate revenue. A stablecoin issuer does not make money by charging users transaction fees like a card network. Instead, it earns by holding reserves—short-term US Treasury bills and cash deposits—against the tokens it issues, and earning interest on those reserves. At scale, this is extraordinarily lucrative. When USDC had $76 billion in circulation and reserves earning around 4.5% in a high-rate environment, the interest income ran into billions of dollars per year. The GENIUS Act, the landmark US federal stablecoin law signed by President Trump in July 2025, codified how these reserves must be held and explicitly prohibited stablecoin issuers from passing that yield on to users. The interest income, therefore, belongs entirely to whoever controls the reserve—the issuer.

This is the asset Circle and Coinbase have been harvesting together. Under a 2023 partnership agreement, Coinbase collects the interest income generated by USDC held on its exchange—100% of it—while splitting revenue 50/50 with Circle for USDC circulating across all off-platform and DeFi ecosystems. In Circle’s 2025 IPO filing, the arrangement was laid bare: Coinbase receives half of what Circle calls the « residual payment base, » the portion of reserve income derived from Treasury and cash holdings backing the stablecoin. Sacra, a market intelligence firm, estimated that Circle generated approximately $1.68 billion in revenue in 2024, up 16% from $1.45 billion in 2023, with USDC in circulation reaching $73.7 billion by Q3 2025. In that same quarter, Circle reported total revenue and reserve income of $740 million, up 66% year-over-year. For context, the reserve income alone at that scale generates more than most financial technology companies.

| Year | Circle Revenue | USDC Circulation |

| 2023 | $1.45 billion | ~$70 billion |

| 2024 | $1.68 billion | $73.7 billion (Q3 2025) |

« The reserve income alone at that scale generates more than most financial technology companies. »

Sacra, market intelligence firm

The GENIUS Act, by banning yield payments to stablecoin holders, ensured this income would not be competed away by rival tokens offering interest to users.

The Acquisition Trail: Building the Stack Piece by Piece

The stablecoin platform Visa, Mastercard, Stripe, and Coinbase are assembling did not appear overnight. It has been built through a series of acquisitions and strategic moves stretching back over a year. The clearest signal was Stripe’s purchase of Bridge, a stablecoin infrastructure firm, for $1.1 billion in late 2024, closing in February 2025. Bridge gave Stripe the technical capability to issue, manage, and settle stablecoin transactions at scale—the plumbing connecting a digital token to the banking system. Mastercard, not to be outdone, agreed in March 2026 to acquire BVNK, a stablecoin payments company, for up to $1.8 billion—its largest digital asset deal and more than double BVNK’s $750 million valuation in a December 2024 funding round. Before landing BVNK, Mastercard explored buying crypto infrastructure firm Zerohash for $1.5 to $2 billion, and Coinbase itself was in talks to acquire BVNK for approximately $2 billion in late 2025.

Visa has quietly built a stablecoin settlement network that already processes real volume. In April 2026, Visa announced it was expanding its stablecoin settlement pilot to nine blockchains, adding Base, Polygon, the Canton Network, Arc, and Tempo to existing support for Ethereum, Solana, Avalanche, and Stellar. The company said the program was running at a $7 billion annualized rate—up 50% in a single quarter. This is not a research project; it’s a production rail processing billions of dollars in settlement every year. Visa’s approach has been to treat stablecoins as settlement infrastructure rather than a consumer product—a way to move money between institutions and merchants without touching the legacy correspondent banking system. Card networks already settle trillions of dollars in value annually; adding a blockchain layer is an engineering challenge, not a conceptual one.

Coinbase, meanwhile, has been running a white-label stablecoin service and a stablecoin payments product for businesses since late 2025. The exchange also holds a dominant position as the primary on-ramp for USDC in the United States, with approximately 67% market share among US crypto exchanges. Its current arrangement with Circle—collecting 100% of interest income on USDC held on its platform and splitting 50/50 on off-platform circulation—generates stable, growing revenue described by management as essentially a royalty on a reserve base they do not control. When the Coinbase-Circle agreement comes up for renewal in August 2026, the question of whether to continue sharing that economics or redirect it toward a proprietary token becomes urgent.

The Distribution Advantage: Why the Coin Is the Easy Part

The most important insight in understanding why the card network consortium is a credible threat to Circle is this: in stablecoins, the technology is commoditized. Tether and Circle solved the engineering problem years ago—a token that holds its dollar peg, redeems on demand, and moves in seconds across multiple blockchains. What neither company built with the same rigor is the distribution layer—the reason merchants accept the token and consumers hold it. USDT circulates primarily through offshore crypto exchanges and in economies where dollar access is restricted. USDC leans heavily on Coinbase as its primary distribution partner in the United States. Neither token sits natively inside a payment terminal at a retail store, inside a bank’s mobile app as a spending account, or inside the checkout flow of an e-commerce platform at global scale.

Visa and Mastercard own that distribution in ways no stablecoin issuer has ever replicated. Visa runs more than 130 stablecoin-linked card programs across over fifty countries. Mastercard’s BVNK acquisition was explicitly framed by its chief product officer, Jorn Lambert, as acquiring tools to chase new addressable markets, with remittances cited directly. Both networks sit between hundreds of millions of merchants and consumers and the banking system—the exact relationship that makes a new token useful the moment it is issued. A stablecoin pre-integrated with those networks does not need to spend years building merchant relationships; it inherits them. For a merchant already processing Visa and Mastercard transactions, adding a settlement option denominated in a network-issued stablecoin requires no new terminal, no new relationship, and potentially lower costs than existing card rails.

The GENIUS Act makes this dynamic sharper. By setting uniform reserve, redemption, and licensing standards, the law turns a compliant dollar token into a commodity—any qualified issuer can produce one to the same spec. Once the token itself is standardized, differentiation shifts entirely to distribution. A consortium coin backed by dominant card networks begins that competition with defaults already set in its favor. Users hold whatever stablecoin their app or bank defaults to, and a coin sitting inside the Visa and Mastercard ecosystems has the most defaults.

Why Circle Is the Most Exposed Incumbent

Circle’s position looks more vulnerable in this context than Tether’s. Tether’s USDT, with approximately $115 billion in circulation, dominates the offshore and emerging market segment—precisely the markets where users want dollar access and cannot or will not use the regulated US banking system. A US-regulated network coin aimed at domestic merchant settlement and institutional settlement may simply not appeal to Tether’s existing customers. The dynamics are different; the use cases are different. Tether’s management has shown no particular interest in competing for the card network’s turf.

Circle is a different story. USDC is the dominant regulated stablecoin in North America and Europe, the geographic markets where card networks have their deepest merchant and consumer relationships. Circle’s listing and institutional branding make it a direct target for the consortium’s positioning. Circle’s stock fell 4% on the consortium news; Coinbase fell in sympathy. The investor reaction was telling: the companies most exposed to the economics of stablecoin reserve revenue are the ones most directly in the crosshairs of this new entrant.

The GENIUS Act also creates a specific structural disadvantage for Circle. Once any qualified issuer can produce a token to the same reserve standard, the early-mover advantage Circle spent years building—its regulatory relationships, banking partnerships, insurance coverage for reserves, compliance infrastructure—becomes the baseline rather than the differentiator. Being first matters less when the race has a defined course and the starting line is open to all comers. Card networks, with existing balance sheets and regulatory relationships with the Federal Reserve and banking regulators, are well positioned to meet those standards quickly.

The Revenue Sharing Architecture: Coinbase’s Delicate Position

One of the most intricate aspects of this story is Coinbase’s position within the emerging landscape. The company currently sits in the unusual role of being both a potential founding member of the consortium and the largest single beneficiary of Circle’s economics. Its 2023 revenue-sharing agreement with Circle—Coinbase keeps 100% of reserve interest on USDC held on its platform and splits 50/50 with Circle on off-platform USDC—has been described by analysts as essentially a perpetual royalty on a reserve base Coinbase does not manage. Bernstein, a brokerage firm, noted in early 2026 that Coinbase’s stablecoin revenue surged nearly 51% in Q1, driven by USDC growth.

« The arrangement has been so favorable to Coinbase that Circle’s management has reportedly been seeking to renegotiate the terms as renewal approaches. »

Analyst reports

Joining a consortium coin would give Coinbase a way to generate reserve revenue on its own terms rather than relying on Circle’s goodwill in upcoming negotiations. A Coinbase-issued stablecoin—even one produced under the consortium framework—would allow the exchange to retain the interest income on its own reserve base rather than sharing it with Circle. At $76 billion in USDC circulating, and with the bulk held on Coinbase’s platform or in its ecosystem, the economic stakes of that transition are enormous. Circle is reportedly considering alternatives, including a renewed push for its own IPO after a prior attempt stalled, and has been building relationships with other exchanges including Binance and Bybit to diversify away from its heavy dependence on Coinbase. The Bybit agreement, which followed the Binance model of splitting reserve yield 50/50, suggests Circle is hedging against the possibility that Coinbase redirects its USDC economics toward a proprietary token.

What Would the Consortium Coin Actually Look Like

The public details of the consortium remain sparse. The CoinDesk report that broke the story in early June 2026 cited three people familiar with the plans, and Fortune subsequently reported that no formal deal may yet exist—possibly not even signed memoranda of understanding. The companies involved—Visa, Mastercard, Stripe, Coinbase—are not known for moving quickly on ventures requiring four-way governance across rival companies with overlapping ambitions. Facebook’s Libra coalition collapsed in 2019 under the weight of exactly the kinds of coordination problems this consortium would face.

The most credible interpretation is that the talks represent genuine strategic interest rather than a finalized plan. The acquisitions—Bridge, BVNK, Visa’s settlement expansion—are concrete and ongoing. The regulatory framework has removed the primary obstacle preventing serious institutional entrants from building in this space before. The GENIUS Act, by setting clear rules, made it possible to build a stablecoin product to a defined spec without years of bespoke legal and compliance work for each state. This clarification alone changes the cost-benefit calculation for any company with the balance sheet to participate.

The most likely near-term product, if the consortium proceeds, is not a consumer-facing token with a consumer brand. It is a settlement and treasury instrument—a stablecoin used by banks and merchants to settle transactions, hold working balances, and manage cross-border flows more efficiently than legacy correspondent rails allow. Card networks have the merchant relationships. Stripe has the technology infrastructure from Bridge and its existing payments platform. Coinbase has the crypto-native liquidity and regulatory positioning. Together, they could offer a product that moves money between financial institutions and merchants at a lower cost and faster speed than the existing system, with the reserve yield accruing to the consortium rather than to a third-party issuer like Circle.

Tokenized Money Market Funds: The Next Layer of the Stack

The consortium’s ambition does not end with a dollar-pegged stablecoin. Wall Street’s largest asset managers have already begun positioning their money market funds as stablecoin reserve infrastructure—a development that would reshape the economics of stablecoin issuance from the ground up. Invesco filed an amended registration statement with the SEC in June 2026 to add the Invesco Stablecoin Reserves Onchain Fund to its Short-Term Investments Trust, explicitly designed to invest in assets that payment stablecoin issuers are permitted to hold under the GENIUS Act framework. BlackRock, the world’s largest asset manager with more than $6 trillion in assets under management, submitted paperwork to debut a digital share class of its existing Treasury-based liquidity fund and a newly created tokenized money market fund aimed at investors who manage their cash through crypto wallets and stablecoins rather than traditional brokerages.

These moves are not competing with the card network consortium—they are complementary. A tokenized money market fund held as stablecoin reserve collateral generates yield accruing to the reserve holder. If card networks control the reserve layer through their own tokens, they also control the choice of which money market fund holds that reserve. Asset managers like BlackRock and Invesco are positioning to be the designated reserve vehicle for a new generation of network-issued stablecoins, turning their existing Treasury expertise into a B2B product rather than a consumer one. The stablecoin issuer controls the token; the asset manager holds the reserves. The revenue from the float is shared between them in whatever arrangement the network negotiates.

The Regulatory Brake: Antitrust and the GENIUS Act’s Own Constraints

The consortium faces meaningful obstacles beyond the difficulty of coordinating four rival companies. The GENIUS Act itself contains provisions that reshape the competitive landscape in ways the card networks will have to navigate carefully. The law favors bank and licensed issuers as the primary permitted stablecoin issuers. A consortium co-owned by the world’s two dominant card networks invites the same antitrust scrutiny regulators have already applied to those networks’ existing market power in card payments. The Federal Reserve, the OCC, and the FDIC have all issued proposed rules in early 2026 implementing the GENIUS Act’s reserve and custody requirements—rules that will determine exactly who qualifies as a permitted issuer and what custody arrangements are acceptable. The structure and timing of any consortium launch will depend significantly on how those rules are finalized.

The existing card networks have also, until recently, been publicly dismissive of the stablecoin threat to their core business. A senior Mastercard executive told analysts less than a year before the consortium talks became public that most stablecoin flows would begin and end in fiat currency and posed no meaningful threat to card rails. A firm that believed its own dismissive messaging has less strategic urgency to cannibalize its existing business model with a competing product. The tension between defending the legacy card business and investing in a disruptive new settlement layer is not easily resolved—particularly when the same executives who run the card networks are also responsible for deciding how aggressively to pursue the stablecoin opportunity.

Outlook: Competitive Pressure Without Certainty

For Circle, the consortium represents the most credible competitive threat to its business model since Tether’s emergence as the dominant offshore stablecoin. The $325 billion stablecoin market is no longer a crypto-native curiosity—it is a regulated, mainstream payments infrastructure layer that traditional finance has decided to enter seriously. The card networks’ acquisition spending alone—$1.1 billion for Bridge, up to $1.8 billion for BVNK, and years of Visa’s internal development—represents a level of capital commitment difficult to walk back from. The GENIUS Act has provided the regulatory clarity that makes the investment case coherent. And the distribution advantages Visa and Mastercard hold are not easily replicated by a company that started as a cryptocurrency issuer rather than a payments network.

The timing of any actual launch remains uncertain, and the consortium model—four large companies with competitive overlaps sharing governance of a new asset—carries genuine execution risk. Facebook’s Libra collapsed under the weight of similar coordination challenges. The history of payments industry consortia is littered with well-reasoned strategies that failed on the road to implementation. But the strategic logic is sound, the capital is committed, and the regulatory path is open. For Circle and for Coinbase, whose revenue from the current arrangement with Circle is substantial and growing, the question is no longer whether this competition will arrive but when—and whether the existing USDC partnership economics can survive the transition to a world where card networks issue their own tokens and control the reserves that underpin them.

Sources

- CoinDesk: Payment giants Stripe, Visa, Mastercard said to be among backers of soon-to-debut stablecoin platform

- Forbes Digital Assets: Why Visa And Mastercard Are Building The Stablecoin That Could Sink Circle

- Fortune Crypto: Visa and Mastercard are planning to shake up the stablecoin market — but pulling it off won’t be easy

- Eco (Support): What Is the GENIUS Act? US Stablecoin Law Explained for 2026

- Sacra: Circle revenue, funding and growth rate

- Decrypt: Coinbase Takes 50% Share of Circle’s Residual USDC Reserve Revenue: Filing

- Yahoo Finance: Invesco Targets Stablecoin Reserves With New Tokenized Money Market Fund

- CoinDesk: Circle Has USDC Revenue Sharing Deal With Second-Largest Crypto Exchange ByBit: Sources

This article is published for informational and educational purposes only. It does not constitute investment advice. Do your own research (DYOR) before making any decisions.