{kind=link}

Since the approval of spot Bitcoin ETFs in January 2024, the crypto investment landscape has rapidly evolved towards more sophisticated solutions. Bitcoin Premium Income ETFs represent the latest iteration: funds that don’t just track Bitcoin’s price, but actively harvest its legendary volatility to generate regular cash flow.

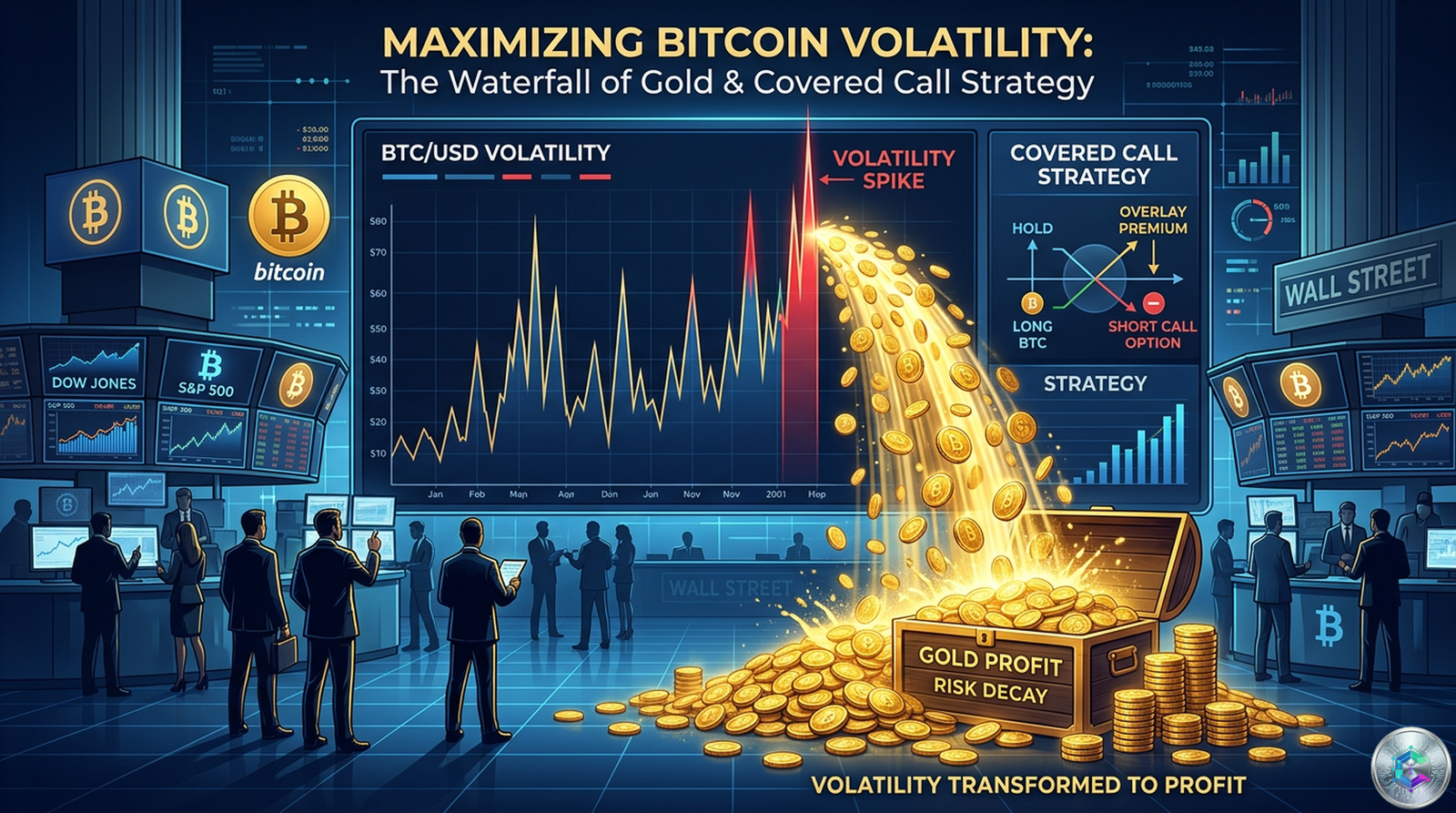

🔑 Key Takeaways

- Premium Income ETFs write covered call options on Bitcoin exposure to collect premiums distributed to shareholders.

- BlackRock, Goldman Sachs, and Grayscale have filed or launched products in this category, signaling growing institutional interest.

- The strategy captures Bitcoin upside at the strike price, offering regular income but capping potential gains.

- Performance shows high annualized yields (25-37%) but total losses in bearish markets.

- Increased market participation could compress volatility premiums, affecting future income.

Understanding Bitcoin Premium Income ETFs

Bitcoin Premium Income ETFs mark a departure from the passive buy-and-hold philosophy of early spot Bitcoin ETFs. Unlike funds like BlackRock’s iShares Bitcoin Trust (IBIT) that hold Bitcoin directly, these products actively write covered call options to generate income. The strategy involves selling call options on held Bitcoin, giving the buyer the right to purchase at a predetermined price. The premium received is distributed to shareholders. In exchange, the fund caps its upside if Bitcoin rises above the strike price, turning volatility into a revenue stream while limiting gains.

Key Players: BlackRock, Goldman Sachs, Grayscale

BlackRock filed in September 2024 for the iShares Bitcoin Premium Income ETF, refiled in January 2026 with a 0.65% annual management fee. The fund holds shares of IBIT (spot Bitcoin exposure) and writes calls on 25-35% of net assets, actively managing strike prices. Goldman Sachs followed in April 2026 with a similar ETF, committing to invest at least 80% of net assets in Bitcoin exposure vehicles, primarily ETPs. Grayscale already offers the Grayscale Bitcoin Premium Income ETF (BPI) on NYSE Arca, using derivatives on ETPs. BPI has paid dividends like $0.1823 per share on May 13, 2026, with a meaningful annualized yield.

« BlackRock built a quarter-billion-dollar business, almost overnight. For comparison, many fintech unicorns don’t make that in a decade. This isn’t experimentation anymore. The world’s largest asset manager has proven that crypto is a serious profit center. »

Leon Waidman, Head of Research at Onchain Foundation

Competitive Landscape and Performance

The market includes several competing ETFs. The Roundhill Bitcoin Covered Call Strategy ETF (YBTC) offers an annualized distribution rate of 35-37%, but a total return since launch of approximately -45%. The Amplify Bitcoin Max Income Covered Call ETF (BAGY) targets 30-60% annualized option premiums with weekly calls, a distribution rate of 37.1% but total return of about -25%. The NEOS Bitcoin High Income ETF (BTCI) has a rate of 27.25% and a return of -31.3%. The Global X Bitcoin Covered Call Strategy ETF (BCCC) with a lower expense ratio of 0.75% shows returns between -24.98% and -32.33%.

| ETF | Annualized Distribution Rate | Total Return Since Launch | Expense Ratio |

|---|---|---|---|

| YBTC (Roundhill) | 35-37% | -45% | 0.95% |

| BAGY (Amplify) | 37.1% | -25% | Not specified |

| BTCI (NEOS) | 27.25% | -31.3% | Not specified |

| BCCC (Global X) | Not specified | -24.98% to -32.33% | 0.75% |

These figures highlight a fundamental trade-off: the income generated comes at a cost. In bullish markets, the funds underperform unhedged Bitcoin due to capped gains. In bearish markets, premiums may not offset losses, especially after fees. In sideways markets, they perform best.

The Volatility Paradox

Bitcoin’s implied volatility, measured by indices like the Volmex BVIV index, currently sits around 40%, with predictions of spikes to 80% in 2026. Higher volatility increases option premiums, boosting distributable income. However, this creates a paradox: income is highest when volatility is strong, often during price stress periods. In a crash, funds generate elevated premiums but suffer losses on underlying positions. Conversely, in calm bull markets, income compresses, but investors partially benefit from price appreciation.

« Bitcoin volatility is already suffering from significant oversupply due to the proliferation of spot ETFs, structured products, and IBIT options. Additional mechanical call-selling could pressure market-implied premiums lower over time, reducing future income for funds. »

Jake Ostrovskis, Head of OTC Trading at Wintermute

Regulatory and Structural Framework

Premium Income ETFs are registered under the Securities Act of 1933, offering more flexibility but fewer protections than funds under the Investment Company Act of 1940. None hold Bitcoin directly; they own shares of spot Bitcoin ETFs, creating layered exposure. For example, BlackRock’s ETF combines a 0.65% fee for the Premium Income fund and 0.19% for IBIT, totaling about 0.84% annually. This operational structure prioritizes regulatory clarity over maximum efficiency.

Are They Right for You?

These ETFs address the need for income generation while exposing to Bitcoin, suitable for portfolios requiring regular distributions like retirement accounts. However, trade-offs are significant: capped upside in strong Bitcoin rallies, potential classification of distributions as return of capital affecting taxes, and complexity of options mechanics. Market dynamics, with possible premium compression, mean income is not guaranteed. For professional allocators, these ETFs are better viewed as a tactical position within a broader Bitcoin allocation, complementary to direct spot exposure.

Implications for the Crypto ETF Market

The proliferation of Bitcoin Premium Income ETFs reflects the mainstreaming of Bitcoin as an asset class within traditional finance. BlackRock and Goldman Sachs’ entries validate Bitcoin’s institutional viability. Using existing ETPs avoids complex custody and reporting requirements. Going forward, the category should expand with more issuers, strategic innovations (like put-spread overlays), and regulatory evolution. Investors must approach these products with clear eyes, understanding they transform Bitcoin risk into a different shape, with regular income but capped upside.

Conclusion

Bitcoin Premium Income ETFs offer a sophisticated response to a real investor need, combining Bitcoin exposure with income generation. For income-focused investors, they provide a way to access crypto while mitigating volatility. However, trade-offs in capped gains, layered fees, and complexity require careful analysis. In a sustained bull market, spot Bitcoin remains preferable for asymmetric exposure. In volatile or sideways markets, Premium Income ETFs can deliver attractive yields. Their adoption will depend on Bitcoin volatility evolution and potential premium compression. Ultimately, they are not a way to avoid Bitcoin risk, but to reshape it for specific income objectives.

Sources

- CoinDesk: BlackRock doubles down on bitcoin fund offerings with income-focused filing

- CryptoSlate: BlackRock launches Bitcoin premium ETF

- CryptoSlate: BlackRock’s new Bitcoin income ETF turns volatility into the product

- CryptoSlate: Why Goldman Sachs wants to turn Bitcoin into an income product

- Arkham Intelligence Research: Everything We Know About Goldman Sachs Bitcoin Premium Income ETF

- Grayscale ETF: Grayscale Bitcoin Premium Income ETF (BPI)

- MarketChameleon: BPI Dividend Information

- Dividend.com: BPI – Grayscale Bitcoin Premium Income ETF

- Amplify ETFs: Amplify Bitcoin Max Income Covered Call ETF (BAGY)

- TotalRealReturns.com: BTCI, YBTC, BCCC Total Return Chart

- PortfoliosLab: BCCC vs. YBTC Performance Comparison

- Reddit r/Bitcoin: Covered call ETFs, anyone compare BTCI, YBTC, and BCCC

This article is published for informational and educational purposes only. It does not constitute investment advice. Do your own research (DYOR) before any decision.