{kind=link}

According to Bitwise CIO Matt Hougan, the era when Strategy single-handedly dictated Bitcoin demand is coming to an end. The STRC mechanism has reached its structural limits, and the market must now rely on a far broader base of institutional buyers.

🔑 Key Takeaways

- Strategy holds 847,363 BTC, roughly 4% of Bitcoin’s total supply.

- The STRC perpetual preferred plunged from $100 to below $75 at the June 2026 low.

- Strategy is now authorized to sell up to $1.25 billion in Bitcoin to shore up liquidity.

- Strategy’s obligations-to-Bitcoin ratio sits at 33%, well below the 50% stress threshold.

- Spot ETFs, pension funds, and sovereign wealth funds are expected to become the next structural drivers of demand.

The rise of Strategy as Bitcoin’s historical buyer

When Michael Saylor first converted a slice of MicroStrategy’s treasury into Bitcoin in August 2020, the move was widely ridiculed. Betting a public company’s balance sheet on a volatile digital asset ran against every tenet of traditional corporate finance. Five years later, that audacity has made Strategy the largest corporate Bitcoin holder on Earth, with a position representing roughly 4% of the supply that will ever be mined.

The bet rested on a straightforward macroeconomic thesis: faced with a supply strictly capped at 21 million units and rising institutional adoption, every dollar sitting idle in a corporate treasury would steadily lose purchasing power. Saylor was not speculating, he argued — he was future-proofing the business. Time vindicated him, at least through the 2024-2025 cycle when Bitcoin repeatedly printed new all-time highs.

But the real innovation was the funding mechanism. From late 2024 onward, Strategy engineered a hybrid capital instrument — the perpetual preferred stock STRC (« Stretch ») — letting it borrow from yield-hungry investors and immediately convert the proceeds into Bitcoin. The dividend, initially set at 8%, was lifted to 11.5% and then 12%, in a market where junk bonds yielded under 7%. The flywheel spun out of control in early 2026: Strategy added $7.2 billion in Bitcoin over just eight weeks, outpacing the combined US spot ETF complex ($3.8 billion over the same window).

The STRC crisis: when the leveraged flywheel stalls

The cracks emerged in late June 2026. Bitcoin, which had clawed its way back to roughly $76,000 in the spring, rolled over as macro headwinds intensified. On June 25, it touched an intraday low of $58,190 — a 21-month floor. For Strategy, a 23% drawdown from recent highs struck at the heart of the mechanism that defined its existence.

STRC collapsed below $75, having traded close to its $100 par value since its July 2025 launch. The mechanism is brutally simple: Strategy’s ability to service a 12% dividend hinges on Bitcoin’s price rising. When the price falls, confidence retreats, and the flywheel reverses on itself.

« In both cases, financial structures attracted capital that depended on unusually favorable market conditions and later had to be unwound before the market could establish a durable bottom. The volatility in STRC is a natural and important part of the crypto cycle. I think we’re nearing the bottom. »

Matt Hougan, Chief Investment Officer, Bitwise

Hougan draws a direct parallel with another inflection point: the implosion of the GBTC premium in 2021, when the Grayscale Bitcoin Trust swung from a small premium to a 30% discount to net asset value as the bull market exhausted itself. At the time, the discount looked like a signal of impending disaster. In hindsight, it marked the end of one cycle and the start of a painful but necessary consolidation phase.

Strategy’s response was swift. The company announced a new capital management framework permitting it to sell up to $1.25 billion in Bitcoin to bolster its dollar reserve, meet dividend and debt obligations, and fund share buybacks. The STRC dividend was held at 12%, and up to $2 billion in common and preferred stock buybacks were authorized. The message is unmistakable: Strategy is shifting from unconditional accumulation to conditional management.

Is Strategy actually at risk? A liquidity analysis

Despite the market panic, Hougan dismisses the idea of imminent liquidation risk. The numbers, he argues, simply do not support that scenario. Strategy holds roughly $52 billion in liquid assets (Bitcoin and cash) against approximately $7 billion in debt and preferred equity obligations.

| Financial Indicator | Value (June 2026) |

|---|---|

| Bitcoin held | 847,363 BTC |

| Share of total supply | ~4% |

| Average purchase price | $66,384 |

| Cumulative investment | ~$33.1 billion |

| Holdings value (at June 25, 2026 price) | ~$49.3 billion |

| Total obligations (debt + preferred) | ~$21 billion |

| Obligations / Bitcoin ratio | 33% |

| Dollar reserve | $2.55 billion |

| Dividend & debt coverage (no new issuance) | ~28 years |

The company has committed to maintaining a dollar reserve sufficient to cover at least 12 months of dividend and interest payments. At current Bitcoin prices, even if Strategy began selling its holdings immediately, it could meet STRC dividends and preferred obligations for approximately 28 years without issuing a single new share or bond. The obligations-to-Bitcoin ratio, currently 33%, leaves meaningful headroom before reaching the 50% level Hougan flags as the zone where investors would start asking hard questions.

Rajiv Sawhney, head of international portfolio management at Wave Digital Assets, shares that view. He notes that the reflexive link between STRC and Bitcoin cuts both ways: « In a calm or rising tape, the flywheel works. In a sharp drawdown, it can reverse quickly. » Matt Cole, CEO of Strive, points out that the 847,363 Bitcoin held by Strategy represent only 4% of total supply — below the SEC’s 5% materiality threshold.

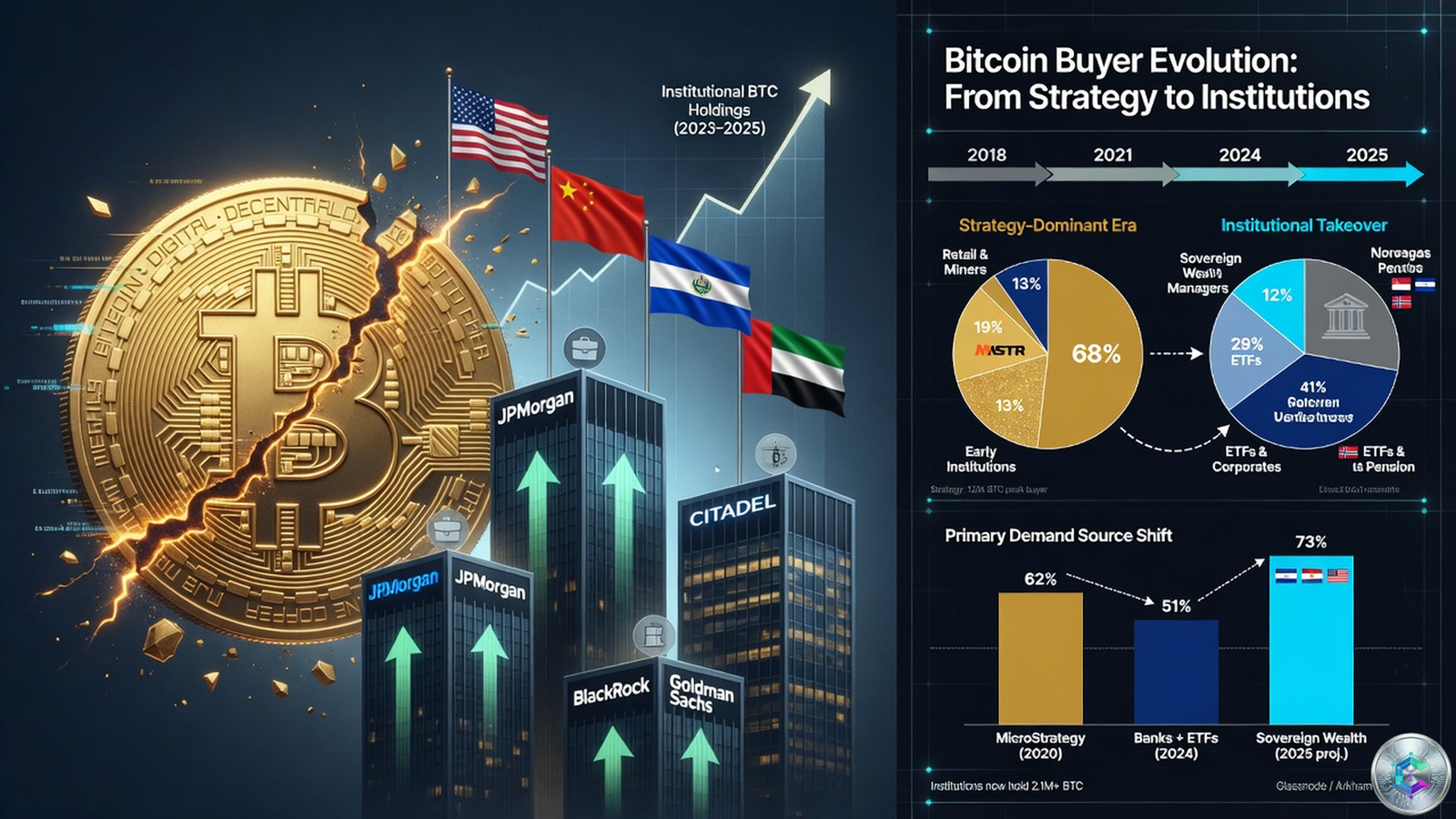

Who steps in? Institutional investors as Strategy’s successor

If Strategy is no longer the dominant buyer, who picks up the baton? The consensus answer points to the broader institutional ecosystem — banks, asset managers, pension funds, university endowments, sovereign wealth funds, and financial advisors.

Several structural factors support this handover. First, regulatory clarity around Bitcoin has improved markedly, with the approval of US spot Bitcoin ETFs in January 2024 providing a compliant, liquid vehicle for institutional allocation. Second, custody and execution infrastructure has matured to the point where large institutions can manage Bitcoin exposure without prohibitive operational complexity. Third, the macroeconomic case for Bitcoin — a hedge against currency debasement, fiscal deficits, and geopolitical risk — has rarely looked stronger.

Early evidence is already visible. In January 2026, the Louisiana State Employees’ Retirement System (LASERS) disclosed a position in Strategy shares — modest (17,900 shares worth roughly $3.1 million, or 0.02% of its portfolio) but symbolically significant. For the first time, a US public pension fund had taken direct Bitcoin exposure via a listed vehicle. Hougan specifically names sovereign wealth funds as a category to watch in the next cycle, despite the political sensitivities that remain in many jurisdictions. The key distinction between this emerging institutional demand and the demand Strategy provided is diversity: Strategy was a single, concentrated, programmatic buyer; institutional demand is dispersed across thousands of decision-makers, structurally more durable but less likely to produce dramatic price effects.

Conclusion

Strategy’s story is one of the most remarkable chapters in modern corporate finance. A mid-sized software company, led by a visionary executive with deep conviction in Bitcoin’s future, used financial innovation to become one of the largest Bitcoin holders on the planet. For five years, it was the single most important marginal buyer in the market, setting prices and sustaining sentiment in ways no other participant could match.

That chapter is closing — not with a collapse, but with a transition. Strategy remains financially healthy, probably healthier than its critics suggest. But its role in the Bitcoin market has fundamentally changed. It is no longer the unconditional buyer that anchored demand: it is becoming what it was always going to become, a large Bitcoin holder managing its position in a complex and changing market. The question is whether what comes next — institutional investors, sovereign wealth funds, pension funds, and the broader ecosystem of financial intermediaries — can pick up the slack in a way that sustains the price and supports the next leg of adoption. If Bitwise’s Hougan is right, the market that emerges from the STRC unwind could lay the foundation for the most significant Bitcoin bull market yet — one built not on the shoulders of a single eccentric company, but on the collective conviction of the global financial system.

Sources

- CoinAcademy.fr — Strategy’s reign as Bitcoin buyer nears its end, per Bitwise

- Sherwood News — Analyst: Strategy has been the single biggest factor for bitcoin’s recent rally

- CryptoBriefing — Bitwise CIO sees new Bitcoin bull market beginning this fall

- BeInCrypto / Yahoo Finance — Bitwise CIO Reveals the Hidden Force Behind Bitcoin’s 20% Rebound

- Bitbo.io — Strategy (MicroStrategy) Bitcoin Holdings Chart & Purchase History

- TheStreet / Yahoo Finance — U.S. pension fund makes surprise buy of Michael Saylor’s Strategy

This article is published for informational and educational purposes only. It does not constitute investment advice. Do your own research (DYOR) before making any decision.