{kind=link}

Tokenized Real-World Asset Market Surpasses $27.6 Billion in April 2026 — An Unexpected Safe Haven Amid Geopolitical Turmoil

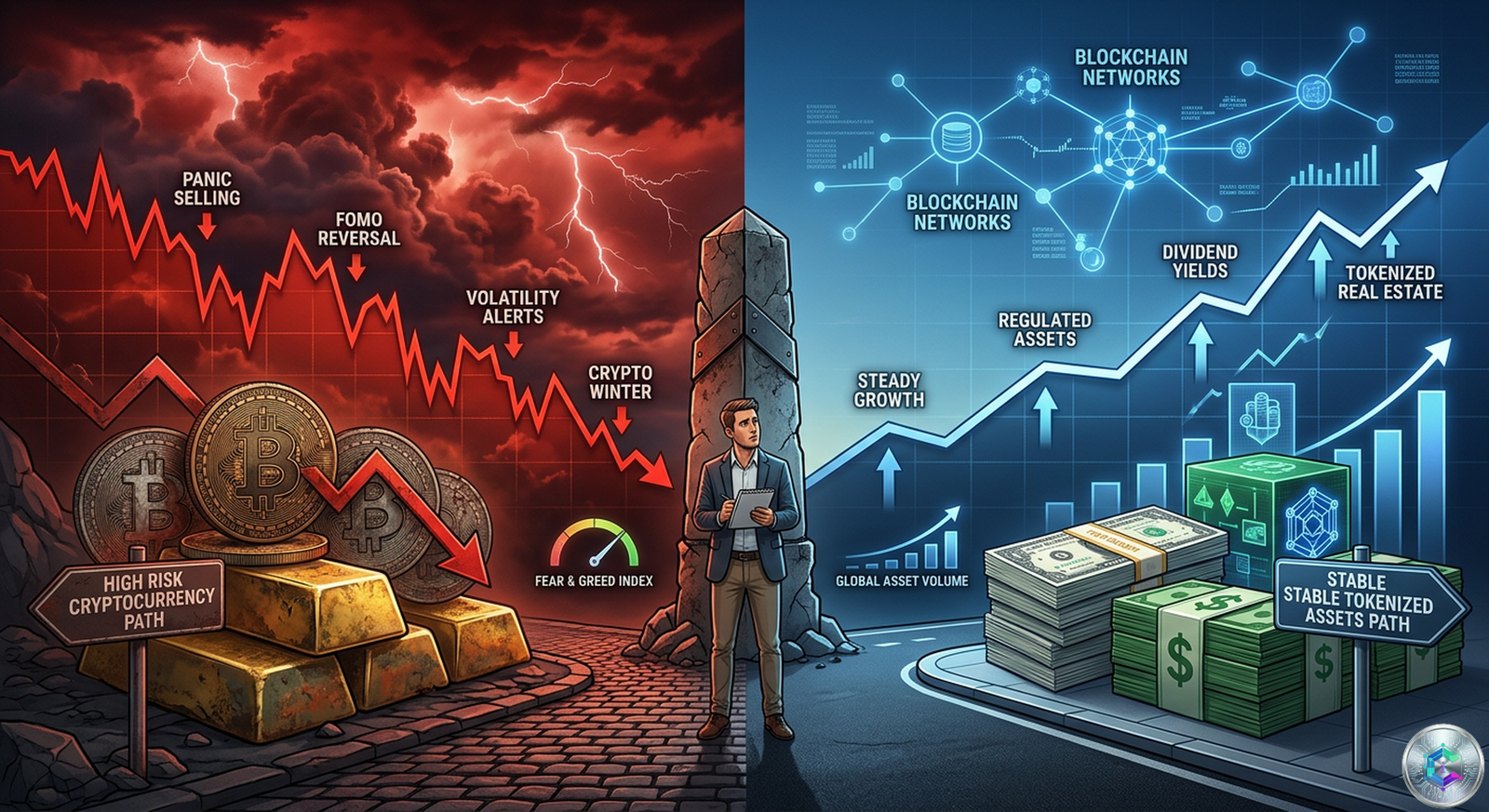

While the cryptocurrency market endures a period of severe turbulence, characterized by pervasive investor fear and persistent downward pressure on Bitcoin’s price, one segment has been remarkably resilient: tokenized real-world assets, commonly known as RWAs. In April 2026, this market reached an impressive $27.65 billion, representing a 4.07% increase despite a broadly unfavorable environment for risk assets. This figure conceals a far deeper dynamic: a silent reallocation of institutional capital toward financial products backed by tangible, regulated assets, providing unexpected stability in the middle of the storm.

A Resilient Market in a Hostile Environment

April 2026 will likely be remembered as a period of striking contrast for the crypto ecosystem. On one side, Bitcoin struggled to maintain price levels above $70,000, with openings around $68,860 in early April and a downward trend that kept traders on edge. On the other hand, tokenized products backed by real-world assets — primarily US Treasury bonds, but also real estate and commodities — continued their upward trajectory, drawing capital fleeing from pure cryptocurrency volatility.

This divergence is far from insignificant. It reflects a structural shift in the way institutional players perceive and utilize digital assets. Far from being abandoned during periods of stress, tokens representing real assets have become preferred instruments for diversification and capital protection. Tokenization brings enhanced liquidity, blockchain-reinforced transparency, and crucially, a significant reduction in counterparty risk — all factors explaining their growing appeal among traditional asset managers.

It is essential to understand that this dynamic is not a short-term phenomenon. The growth of the RWA market is part of an underlying trend that has accelerated over the past 18 months, driven by improvements in technical infrastructure, the emergence of more sophisticated tokenization protocols, and above all, renewed interest from major financial institutions in digital assets. BlackRock, Franklin Templeton, JPMorgan, and numerous other leading asset managers have launched their own tokenized products, conferring on this segment an institutional legitimacy it had never previously known. This progressive institutionalization of the RWA market has contributed to attracting a steady flow of new capital, even in the most challenging periods for the crypto sector as a whole.

US Treasuries: The Engine Driving RWA Growth

At the heart of this growth are tokens backed by US Treasury securities, which constitute the primary engine of the RWA market. These instruments allow investors to access yields close to those of traditional bond markets while benefiting from the liquidity and programmability offered by blockchain. In a period of increasing geopolitical uncertainty, US dollar-denominated assets retain their status as the ultimate safe haven, and the tokenization of these securities now enables institutional investors worldwide to access them more easily, without the traditionally associated constraints of regulated capital markets.

The current macroeconomic context, characterized by escalating geopolitical tensions between the United States, Israel, and Iran, has exacerbated risk-off sentiment across global financial markets. Threats of targeted strikes and economic retaliations have created an atmosphere of anxiety that has pushed many investors to liquidate their positions in the most volatile assets, among which Bitcoin naturally featured. Paradoxically, it is precisely in this unfavorable context that RWAs found their clearest justification: offering a stable, regulated alternative for those wishing to remain exposed to the blockchain ecosystem without bearing the full weight of cryptocurrency volatility.

Treasury-backed tokens, such as those issued by protocols like Ondo Finance or Mountain Protocol, have seen their assets under management grow exponentially over recent months. These products typically offer an annual yield in the order of 4 to 5%, directly linked to the federal funds rate, while enabling 24/7 access with minimum investment amounts considerably lower than those required to invest directly in primary bond markets. This democratization of access to US Treasury securities represents a major financial innovation, whose implications for the structure of global financial markets are still difficult to fully measure.

Bitcoin Facing the $100,000 Reality Check

One of the most notable developments of this April 2026 is the drastic reassessment of Bitcoin’s prospects. While many analysts had predicted a surge toward $100,000 before the end of the first half of 2026, prediction markets associated with Bitcoin’s price paint a far grimmer picture. The implied probabilities of reaching that milestone by June 30, 2026, remain extremely low, a situation reflecting the direct impact of geopolitical tensions on investor risk appetite.

This situation is reminiscent of previous Bitcoin cycles, where major macroeconomic and geopolitical events had temporarily derailed well-established bullish trends. However, the most attentive observers note that the market structure has profoundly evolved since the last cycles. The massive entry of institutional players through spot ETFs has altered price dynamics, making Bitcoin more sensitive to regulated capital flows than to speculative movements from retail traders. This relative maturity of the market means that consolidation periods may be longer and more pronounced than previous cycle history suggested.

Bitcoin’s price level, holding within a range between $60,000 and $70,000 for several weeks, perfectly illustrates this impasse. Buyers intervene at each attempt at significant decline, but volumes remain insufficient to sustain a durable upward movement. This technical configuration, characterized by progressively eroding higher highs and lower lows, is often a precursor sign of a more pronounced directional move, although direction remains undetermined. Experienced traders are closely watching key support levels at $62,000 and $58,000, whose breach would open the door to potentially problematic bearish acceleration for long positions.

Institutional Indifference: A Revealing Contrast

One of the most striking characteristics of the current period is the notable absence of major institutional capital inflows into the Bitcoin market. While Bitcoin-based ETF products experienced spectacular introductions in previous years, investment flows have remained desperately weak since the beginning of the geopolitical tensions period. This institutional lukewarmness stands in stark contrast to the enthusiasm that accompanied the first months of spot ETF approvals, raising legitimate questions about Bitcoin’s ability to recover to higher price levels without active support from major market players.

This situation highlights an interesting paradox: the same reasons that push some investors toward RWAs — namely the search for stability and predictability in an uncertain environment — also explain why Bitcoin, despite its theoretical potential, suffers from a lack of short-term confidence. Asset managers have clear mandates regarding risk management, and the volatility observed in cryptocurrencies since the outbreak of Middle Eastern tensions simply does not match the risk profiles they are authorized to take. Consequently, flows that could have supported Bitcoin have veered toward instruments perceived as safer, creating a vicious cycle of selling pressure and disinterest.

Spot Bitcoin ETF flow data is particularly telling. After months of record net inflows that had helped propel Bitcoin to new all-time highs, flows have stabilized at negligible levels, or even slightly negative. This stabilization occurs precisely when the market would need renewed support to maintain current price levels. Without a regular supply of fresh capital, Bitcoin finds itself vulnerable to more erratic price movements, dependent solely on retail trading dynamics that, by nature, tend to amplify movements in both directions.

RWAs as a Credible Alternative: A New Narrative

In this context, tokenized real-world assets offer a value proposition that precisely meets the market’s unmet needs. For institutional investors, the tokenization of real-world assets represents a unique opportunity to combine the advantages of blockchain technology — transparency, liquidity, operational efficiency — with the inherent stability of underlying assets. Tokens backed by US Treasury bills offer regulated, dollar-denominated bond yields, with the convenience of a digital asset. It is this dual attractiveness that explains the sustained growth of the segment, even when the rest of the crypto market traversed a period of difficulty.

Beyond Treasury bonds alone, the tokenization market is progressively extending to other asset classes. Tokenized real estate assets now make it possible to divide ownership of commercial buildings among numerous investors, democratizing access to premium real estate. Platforms like RealT or Lofty already enable investment in US real estate properties with token fractions representing as little as a few tens of dollars, making accessible a market historically reserved for institutional investors or wealthy individuals. This tokenization of real estate introduces new liquidity into a traditionally illiquid market, with profound implications for real estate asset pricing and capital market structure.

Tokenized commodities, from gold to oil, and from silver to rare metals, offer diversified exposures with significantly reduced transaction costs compared to traditional mechanisms. Tokenized gold, represented by tokens like PAX Gold or Tether Gold, allows investors to access the precious metal with near-zero storage and transaction fees, while retaining the ability to instantly convert to liquidity on secondary markets. This operational efficiency represents a significant advance over physical gold products, whose liquidity can be limited and transaction costs high. This progressive diversification of tokenized underlying assets hints at an RWA ecosystem whose capitalization could grow substantially further in the years ahead, as new segments open up to tokenization.

The Federal Reserve’s Role in Future Trends

The question now is under what conditions the cryptocurrency market could regain its momentum. Observers generally agree on two potential triggers: a de-escalation of current geopolitical tensions, or a shift in the Federal Reserve’s monetary policy stance toward a more accommodative, or dovish, approach. Either of these outcomes would be likely to reduce the prevailing risk-off sentiment and free capital currently parked in safe-haven assets to be reallocated toward riskier but potentially more rewarding investments.

The Fed finds itself at a critical juncture in its monetary policy cycle. Inflation, although declining from its 2022 and 2023 peaks, remains above the institution’s 2% target, limiting its room for maneuver for aggressive rate cuts. At the same time, global trade tensions and geopolitical uncertainties weigh on economic growth prospects, creating a complex situation where the Fed must balance its price stability mission with the need not to stifle an economy increasingly exposed to external shocks. The upcoming communications from Jerome Powell and his FOMC colleagues will therefore be scrutinized with particular attention by markets seeking clues about the likely direction of monetary policy in the months ahead.

Current interest rate levels remain a determining factor in the relative attractiveness of different financial assets. With real rates still slightly positive after accounting for inflation, risk-free assets like Treasury bonds continue to offer attractive yields, which naturally restrains rotation toward riskier assets like cryptocurrencies. A significant loosening of monetary policy, which would see key policy rates decline rapidly, could change the game by making cryptocurrencies relatively more attractive compared to risk-free assets. However, such an evolution remains contingent on a normalization of geopolitical conditions and a lasting reduction in inflation — two conditions that appear difficult to achieve in the short term.

A Paradigm Shift for the Crypto Ecosystem

Beyond short-term price fluctuations, the growth of the RWA market represents a significant paradigm shift for the entire cryptocurrency ecosystem. Long criticized for excessive volatility and an absence of links to the real economy, the crypto sector today demonstrates its capacity to serve as a vector for financial innovation by bringing traditional assets closer to the possibilities offered by blockchain technology. This evolution is all the more significant as financial regulators worldwide are actively working to establish legal frameworks for digital assets, thereby creating the conditions for deeper integration between traditional finance and decentralized finance.

The implications of this trend are vast. For issuers of tokenized assets, access to a global and decentralized investor base represents an unprecedented source of liquidity. For investors, the ability to access asset classes traditionally reserved for institutions with considerably lowered investment thresholds opens considerable opportunities. And for the crypto ecosystem as a whole, the presence of financial instruments backed by real assets contributes to legitimizing the entire sector among traditional financial players, thereby facilitating broader long-term adoption.

It is also worth highlighting the potential impact of tokenization on the operational efficiency of financial markets. Blockchain enables real-time settlement, eliminating the T+2 or T+3 delays that characterize traditional financial markets. Smart contracts can automate the payment of dividends, interest, and capital returns, drastically reducing administrative costs and error risks. These efficiency gains, compounded over time, could fundamentally transform the way financial markets operate, ultimately benefiting end investors.

The Fear and Greed Index: 46 Days in Extreme Fear

One indicator that perfectly illustrates the current market mindset is the Fear and Greed Index, which has remained stuck in extreme fear territory for no fewer than 46 consecutive days. This historically low level of market sentiment translates into a particularly pronounced risk aversion among market participants. Historically, extended periods spent in extreme fear territory have often preceded significant rebounds, as they correspond to accumulation phases by the most savvy investors who buy when the majority is selling. However, rebound attempts recorded in recent weeks have resulted in successive failures, with each rally quickly sold off by investors eager to reduce their positions.

This technical configuration, combined with such depressed market sentiment, suggests that the bottoming process could be longer than previous cycles had implied. Investors should prepare for an extended period of volatility and uncertainty, during which patience will be a cardinal virtue. Those with sufficient liquidity to wait could find current price levels an interesting accumulation opportunity, provided they properly calibrate the size of their positions and maintain adequate cash reserves to weather a possible extension of the bearish period.

Geopolitical Risks and the Iran-Israel Tension

The geopolitical dimension deserves special attention in any analysis of the current market situation. The conflict involving the United States, Israel, and Iran has introduced a level of uncertainty that traditional market analysis frameworks struggle to fully incorporate. Financial markets hate uncertainty, and the potential for this conflict to escalate into a broader regional confrontation has weighed heavily on risk asset prices across the board. Beyond the immediate humanitarian and political implications, the conflict carries significant economic consequences that directly affect cryptocurrency markets.

Oil price volatility, a potential disruption to global shipping routes, and the broader implications for global trade have all contributed to a risk-off environment that favors traditional safe-haven assets over speculative instruments. The cryptocurrency market, despite its growing institutional character, still retains a significant speculative component that makes it particularly sensitive to shifts in global risk appetite. Until there is a credible path toward de-escalation, this sensitivity is likely to persist, limiting the ability of Bitcoin and other cryptocurrencies to mount sustained recoveries.

Outlook and Conclusion

The tokenized real-world asset market demonstrated remarkable resilience in April 2026, reaching $27.65 billion in an environment otherwise hostile to most risk assets. This performance underscores tokenization’s capacity to transform traditional assets into attractive digital instruments, capable of attracting capital even during periods of geopolitical stress. For Bitcoin and the broader crypto ecosystem, the path to new records necessarily runs through an improvement in the macroeconomic and geopolitical context, or through a shift in monetary policy by the Federal Reserve.

Until either of these conditions materializes, traders and investors will exercise caution, as evidenced by the weak trading volumes on Bitcoin price prediction markets. Monitoring geopolitical developments and Fed communications will therefore remain essential for anyone seeking to anticipate a trend reversal in cryptocurrency markets. In the meantime, tokenized real-world assets continue their quiet ascent, building the foundations of a more mature, more diversified, and ultimately more resilient digital financial ecosystem capable of withstanding the storms that regularly roil speculative markets.

The growth story of RWAs is probably only just beginning. With the expected entry of new institutional issuers, the opening of new asset classes to tokenization, and the continuous improvement of regulatory frameworks around the world, the medium and long-term growth prospects for this market remain extremely promising. Wise investors would do well to inform themselves about the opportunities offered by this rapidly evolving segment, which may well represent one of the most significant developments in the history of digital finance.